Changes to Loan Level Price Adjustments: What You Need to Know

Learn about the upcoming changes to loan level price adjustments (LLPA) that could impact your mortgage payments starting May 1.

Buying a home is a significant financial decision, and it's important to stay up to date on the latest changes in the industry. Recently, there has been confusion and concern among mortgage borrowers regarding changes to the loan level price adjustment (LLPA) fee structure, with some suggesting that lowering their credit score could lead to a better deal. However, it's important to separate fact from fiction. In this blog, we'll break down the latest changes to the LLPA and how they could impact your mortgage payments.

The Current State of LLPA Fees

The LLPA is a fee charged by lenders to borrowers based on their credit score, down payment amount, loan-to-value ratio, and other factors. The fee can vary depending on the loan program and the individual lender. The LLPA is imposed by Fannie Mae and Freddie Mac, the two entities that guarantee a vast majority of new mortgages. These entities have a mission to promote affordable homeownership, and the Federal Housing Finance Agency (FHFA) announced updates to the Enterprises’ Single-Family Pricing Framework in January to achieve this. To review the previous version of the LLPAs you can view this guide which was in effect until May 1, 2023.

The LLPA Changes Effective May 1, 2023

Earlier this year, the FHFA announced updates to the LLPA structure starting on May 1, 2023. However, the change is only a tweak of an existing fee structure in favor of those with lower credit scores. Intentionally lowering one's credit score will not result in a lower fee. Note that the changes will impact purchases more than refinances, with borrowers with lower credit scores seeing a greater improvement in their loan fees.

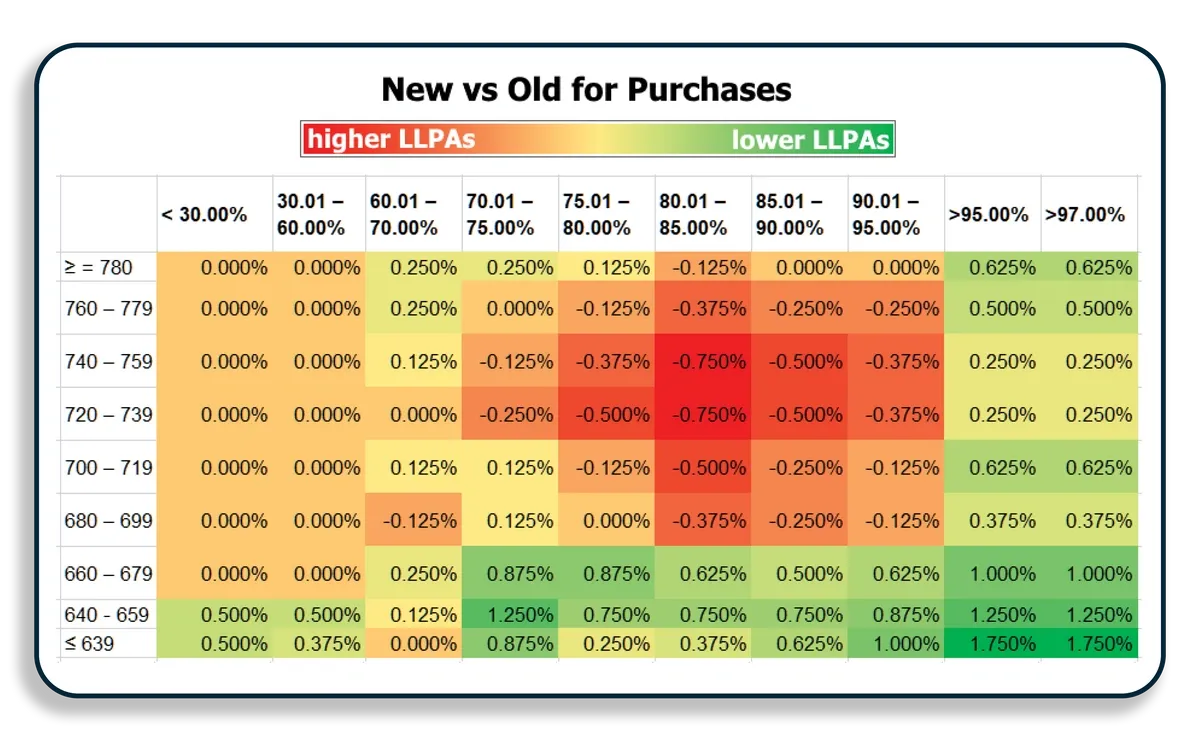

According to Mortgage News Daily, the effective penalty for having a credit score under 680 is now smaller than it was. However, it still costs more to have a lower score. For instance, if you have a score of 659 and are borrowing 75% of the home's value, you'll pay a fee equal to 1.5% of the loan balance, whereas you'd pay no fee if you had a 780+ credit score. But before these changes, you would have paid a whopping 2.75% fee. On a hypothetical $300k loan, that's a difference of $3750 in closing costs.

Borrowers with higher credit scores will generally be paying a bit more than they were under the previous structure. The changes will vary depending on the specific loan program and lender, and some lenders may choose to implement different LLPA fees based on their own internal risk models.

Source: Mortgage News Daily. The chart above shows the differences. Green and yellow cells show where things have become more affordable than they were. Dark orange and red cells = more expensive. All values refer to a percentage of the loan balance charged as an upfront fee.

How Borrowers Can Minimize the Impact of the Changes

It's important for borrowers to shop around, compare rates and fees from multiple lenders, and work closely with their lenders to determine what the new LLPA fees will be and how they can minimize their impact.

The process can be made easier with the help of an experienced real estate agent to guide you through the buying or refinancing process, provide access to reputable industry resources like lenders, and help you make informed decisions about your mortgage. Contact us today at realtor@realtysanantonio.com or call 210-361-6000 to learn more about how we can help you buy or sell your home with ease.

Related Articles

to Top