San Antonio Turns Toward a Buyer's Market

The dial turns further toward a buyer’s market as homes begin selling for 95% of their original asking price.

Whether you are a current or prospective homeowner or renter, and regardless if you are considering buying or selling, it is important to know how the current state of the market impacts your daily decisions while living in San Antonio. We understand the importance of providing you with a transparent outlook on the health of the local market so that you can make informed real estate-related decisions. Our monthly blog is here to provide you with the data to create clarity.

What’s in This Issue?

This month’s market report blog covers the following questions on everyone’s mind. Read below to gain valuable market insights and connect with one of our local agents today!

- Are market conditions more favorable towards buyers?

- What caused the growth in housing inventory?

- Will there be more inventory in 2023?

- Is it a good time to sell?

- Is buying a home still a good investment?

- Will mortgage rates come back down?

After a decade of low-interest rates and rising home values, 2022 continues to be a year of transition. Spiked mortgage rates and elevated prices have moderated the peak frenzy of buyer demand (pending listings), which has slowed the pace of sales. As the pace of sales has eased, the inventory has grown.

What Caused the Growth in Housing Inventory?

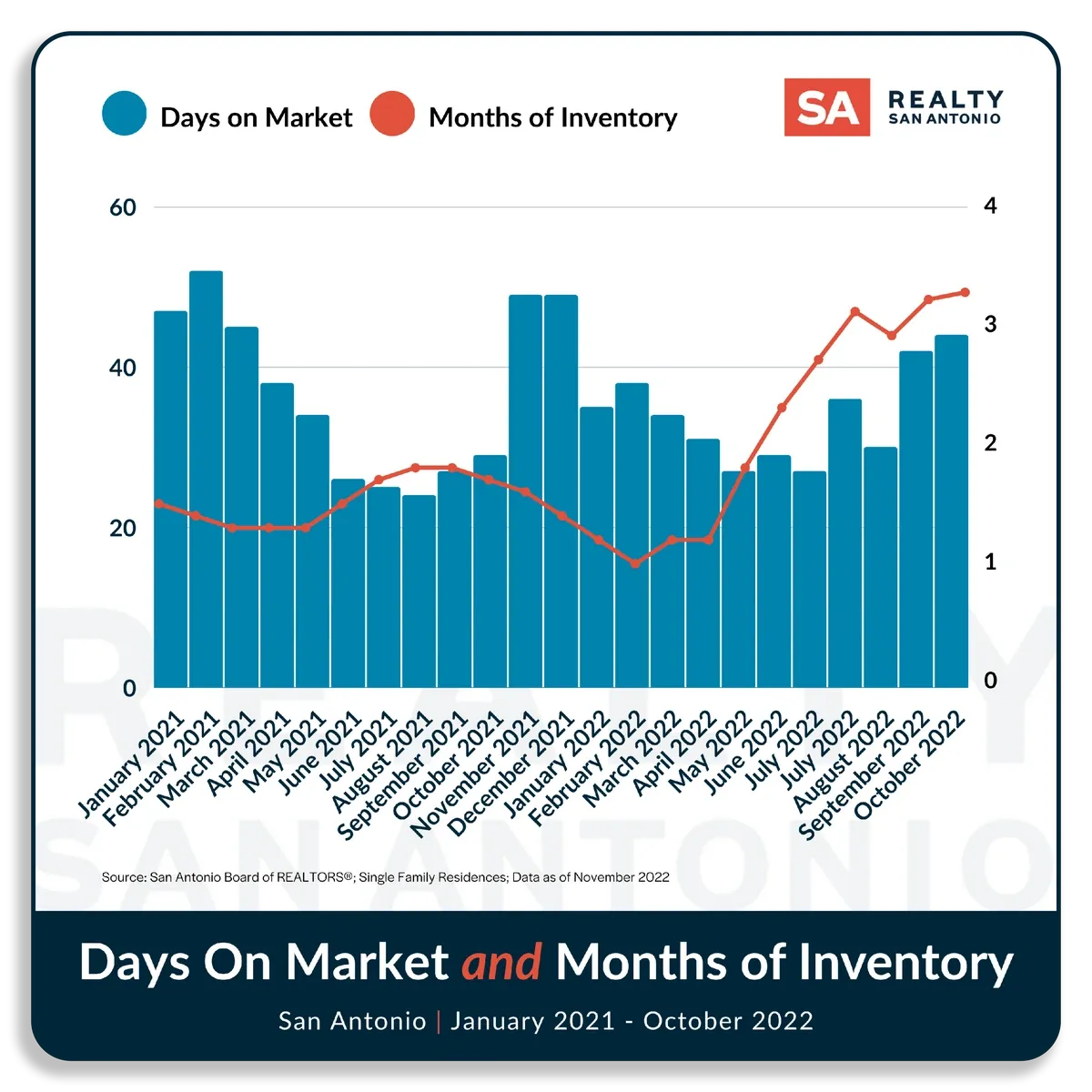

The growth in housing inventory was caused by an influx of recent homeowners listing their homes for sale (new listings) and homes are staying on the market longer (active listings). In October, homes averaged 44 days on the market in San Antonio.

Months of Inventory & Average Days on Market (2021-2022)

Source: San Antonio Board of REALTORS®, All MLS

Inventory has risen quickly, with the number of homes on the market for sale increasing 81% year over year. However, this is beginning to flatten as the number of new listings slowed seasonally, and listings withdrawn from the market surged up 148% from a year ago. Additionally, pending sales fell 32% compared to a year ago, so unsold inventory (active listings) will take more months to absorb. With sales activity tumbling 19% compared to this time last year, monthly inventory levels increased to 3.2 months, up 1.5 months compared to October 2021.

New, Active & Pending Listings (2021-2022)

Source: San Antonio Board of REALTORS®, All MLS, Single Family Residences

The Dial Turns Further Toward a Buyer's Market

Source: Altos Research, Market Action Index for San Antonio, November 28, 2022

Of the over 10,526 homes for sale, in the San Antonio area, 1,200 homes have reduced their price in the past 30 days, and homes sold for 95% of the original asking price compared to 99% a year ago. These are key indicators we are moving towards a Buyer’s Market.

Original List Price vs. Sold Price (2021-2022)

Source: San Antonio Board of REALTORS®, All MLS

Source: San Antonio Board of REALTORS®, All MLS

Will There Be More Inventory in 2023?

It is not likely there will be such an influx of inventory in 2023. There are a record number of equity-rich homeowners who bought or refinanced during the past few years who likely have once-in-a-lifetime low mortgage rates that many owners will not want to give up. Higher financing with a steeper interest rate may not be attractive to homeowners, even with proceeds from the sale of their current home. Economists at Fannie Mae are calling this the “lock-in effect” and expect this trend to remain in a way that has not occurred in over 40 years.

“Economists at Fannie Mae expect home sales to plummet next year to the lowest levels since 2008 before rebounding and helping lead the country out of a brief recession. But the strength of the rebound could be subdued, in large part because so many homeowners will be reluctant to give up the low rates on their existing mortgages,” as reported by Inman News.

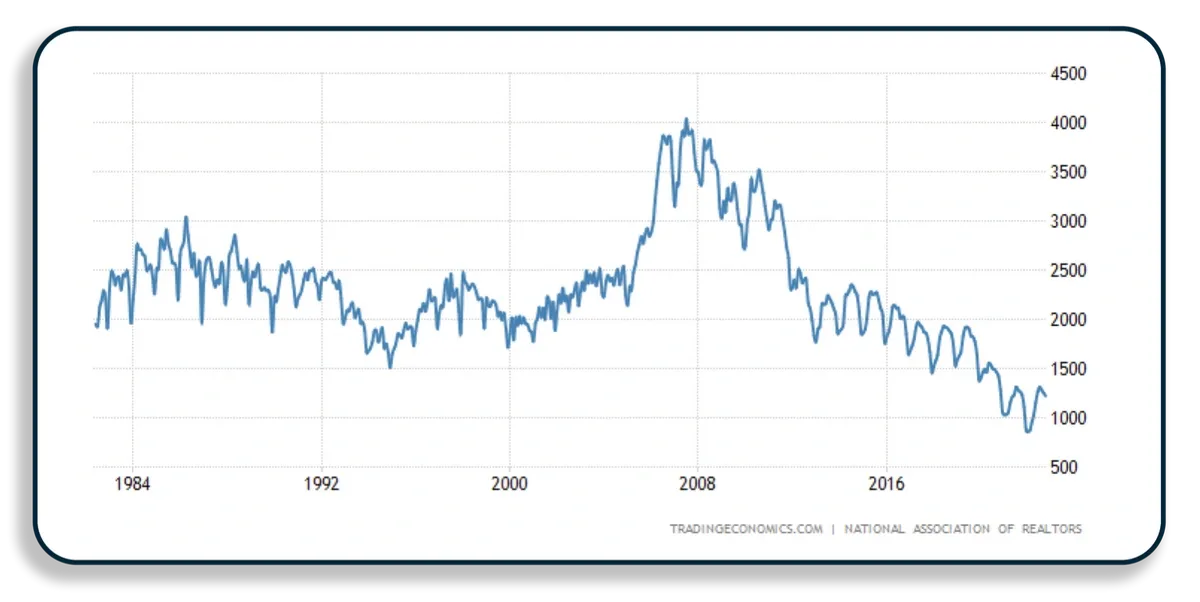

To put housing supply into perspective, the following chart zooms out to show the last 40 years. You can see inventory is still historically low.

PRO TIP: You haven’t missed your window if you want to sell. With inventory still historically low, listing now will allow you to get the jump on other sellers who might be holding off until after the holidays and the start of the new year.

Is Now Still a Great Time to Sell?

The market, and therefore the rate of appreciation, may be slowing down, but that doesn’t mean it’s a bad time to sell. You may have more equity in your current home than you realize - the significant gains in equity by homeowners over the past few years can make a big difference in what you can afford. If you’re thinking about selling your house, connect with a real estate expert so you have the insights you need to make the best possible move today. Homes in San Antonio appreciated 5% compared to a year ago.

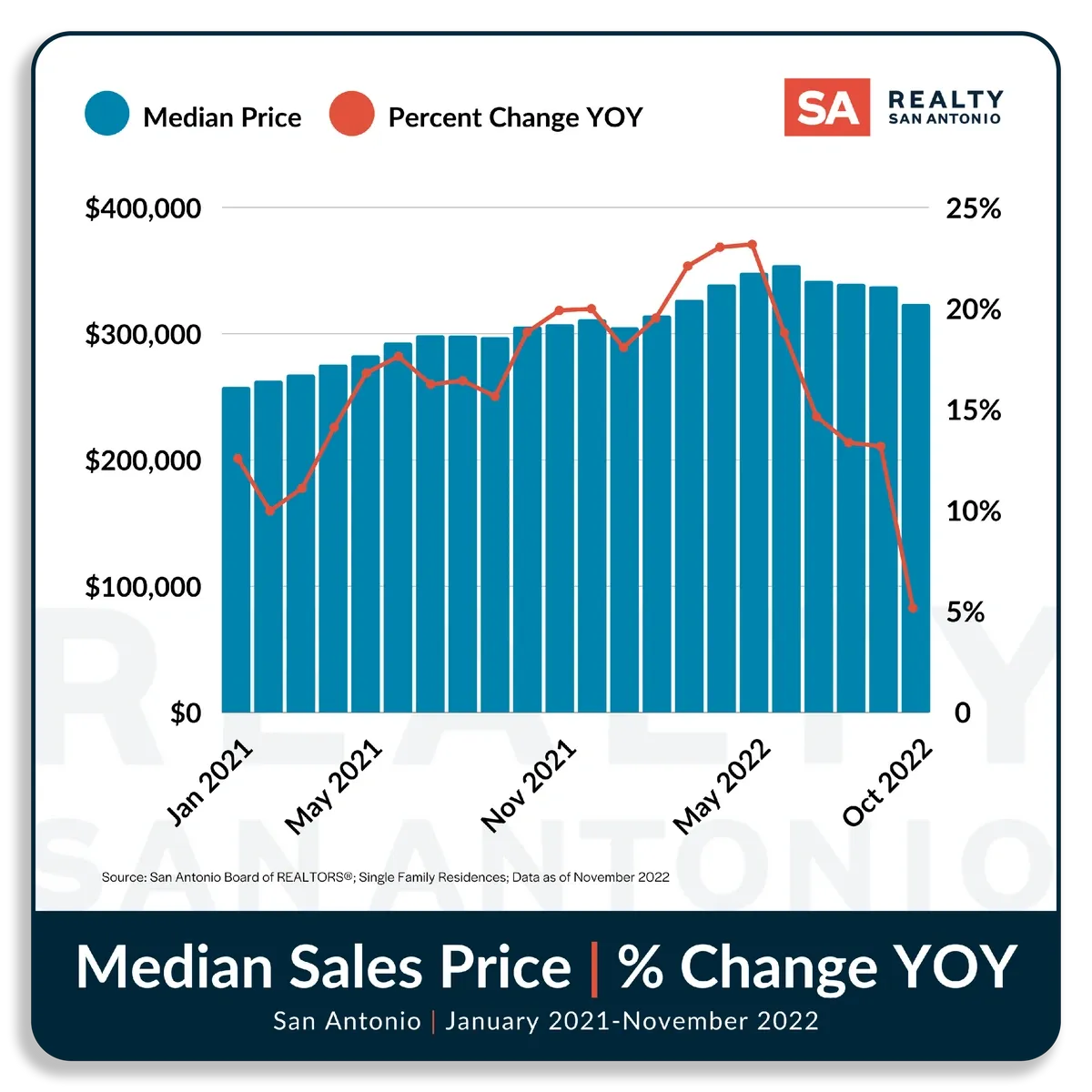

Median Sales Price and Percent Change Year Over Year

Source: San Antonio Board of REALTORS®, All MLS.

Source: San Antonio Board of REALTORS®, All MLS.

As inventory climbs, median prices have receded for the fourth month in a row to $323,190 in October, down 4% from September 2022 and up 5% compared to a year ago.

While buyers may have more leverage in negotiations, sellers are not feeling compelled to sell. There was a 148% increase in withdrawn listings in October compared to a year ago. Many sellers who cannot sell at the price they want are withdrawing their homes from the market instead of panic selling at a lower price. The increase in withdrawn listings may help slow down the decline of falling prices.

Withdrawn & Expired “Off Market” Listings (2019-2022)

Source: San Antonio Board of REALTORS®, All MLS

PRO TIP: The key to success today is being realistic and working with a trusted real estate advisor who can help you set your expectations based on where the market is now, not last year. Sellers will need to price their homes competitively and make their listings stand out to attract online home buyers.

Is Buying a Home Still a Good Investment?

Forbes reports yes, it is still a good investment to buy a home, and home prices are dropping. Here’s why:

Hedge Against Inflation and Long-Term Appreciation

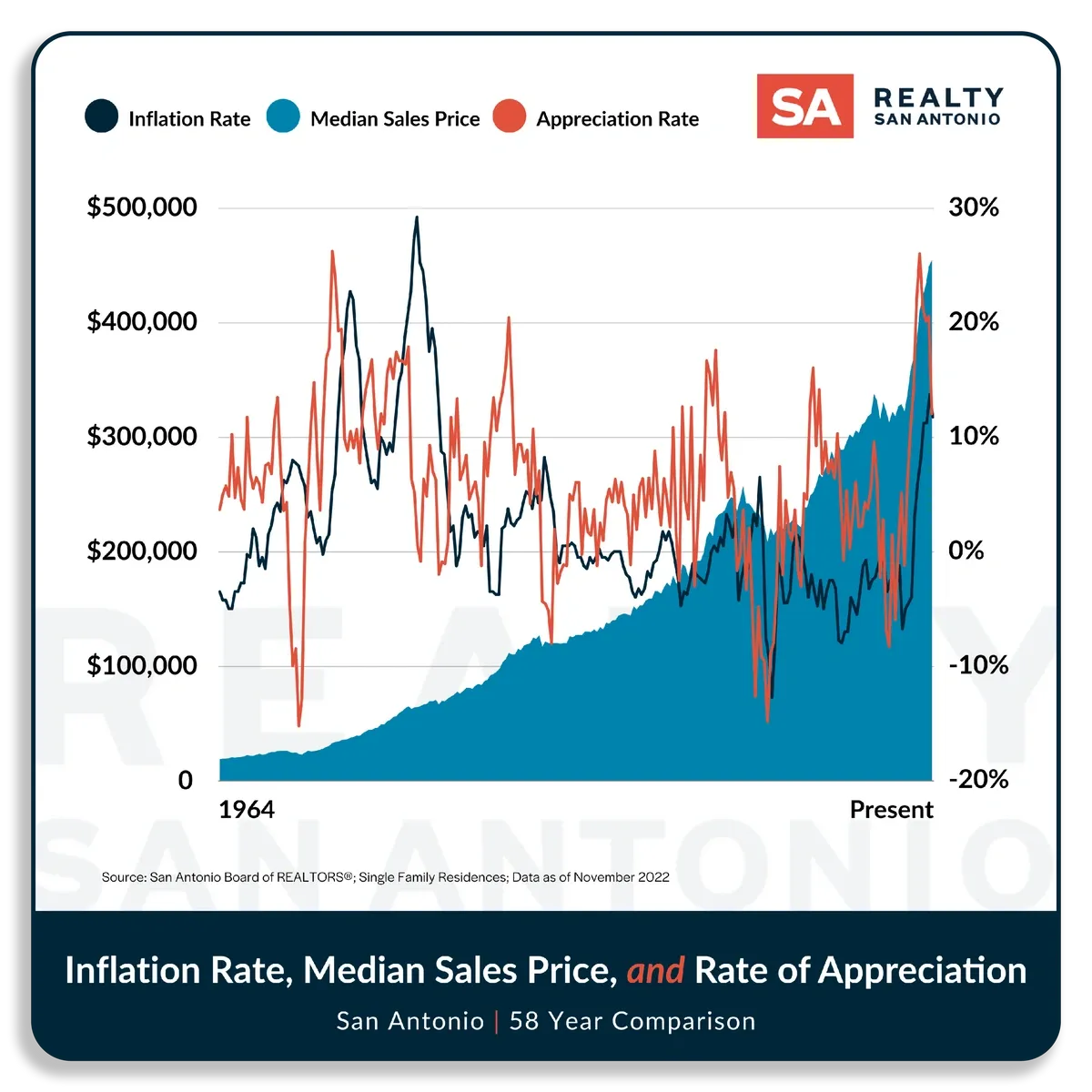

Historically, home price appreciation has outpaced the rate of inflation. There are years, like 2022, when inflation outpaces home price appreciation. But when you zoom out to look at a longer timeframe, the return you earn from home ownership tends to be higher. Traditionally, housing prices trend upwards, with the average annual increase in home values being roughly 4%.

Inflation Rate, Median Sales Price, and Rate of Appreciation (1964-2022)

Source: U.S. Inflation Calculator, FRED Economic Data, St.Louis Fed

Source: U.S. Inflation Calculator, FRED Economic Data, St.Louis Fed

While there is a risk of prices flattening and/or falling in the short term, we don’t expect a severe decline like in 2008. No one has a crystal ball to know when rates will come down, but we do know when rates come down, it will put upward pressure on pricing.

Build Your Equity

The principal from your mortgage payment builds equity every month. If you’re questioning whether to buy a home due to today’s cooling market, consider the long-term financial benefits. As a homeowner, equity increases your wealth.

Gain Tax Benefits

You can receive mortgage interest deductions where you can write off the interest you pay per your tax bracket.

PRO TIP: The Mortgage Reports states, “The idea that you have to put 20% down on the house is a myth.” The truth is you may be able to get grants or low to no-interest loans to help with your down payment or closing costs. It is worth checking to see if you qualify. Down Payment Resource, a company that tracks these programs across the country, makes it easy for you to search programs and check your eligibility quickly.

Mortgage Rates Will Continue to Respond to Inflation

As long as inflation is high, we’ll see higher mortgage rates. The Optimal Blue Mortgage Market Indices, which are updated daily, show a little relief in rates for 30-year fixed-rate loans averaging 6.58% on November 22, down 58 basis points from a 2022 high of 7.16% on Oct. 24, marking the biggest weekly decline in nearly 41 years.

The 10-year yield is going down after the recent muted inflation data, but cooler price growth must become a trend before officials take their foot off the brakes. While “hikes will roll on” the pace may slow, Federal Reserve Governor Christopher Waller said. For the last 30 years, the spread between the 10-year treasury yield and the 30-year fixed rate mortgage has been 1.7 on average.

30-Year Fixed Rate Mortgage Average and 10-Year Treasury Yield (1975-2022)

Source: FRED, 30-Yr Fixed, 10-Yr Treasury Yield

A return to a normal spread between the government borrowing rate, 10-year treasury yield, and the home purchase borrowing rate will bring the 30-year mortgage rates down to around 6%, according to Lawrence Yun, Chief Economist at NAR.

The current spread of 2.8 is larger than the 50-year 1.7 average spread because mortgage companies are charging more as they know the mortgages are going to get refinanced once the rates come back down.

Will Mortgage Rates Come Back Down?

Rates will come down - it’s just a matter of time, and when they do, it will improve affordability for prospective home buyers. Mortgage demand has been up for the third week in a row as rates continue to ease from their 2022 highs.

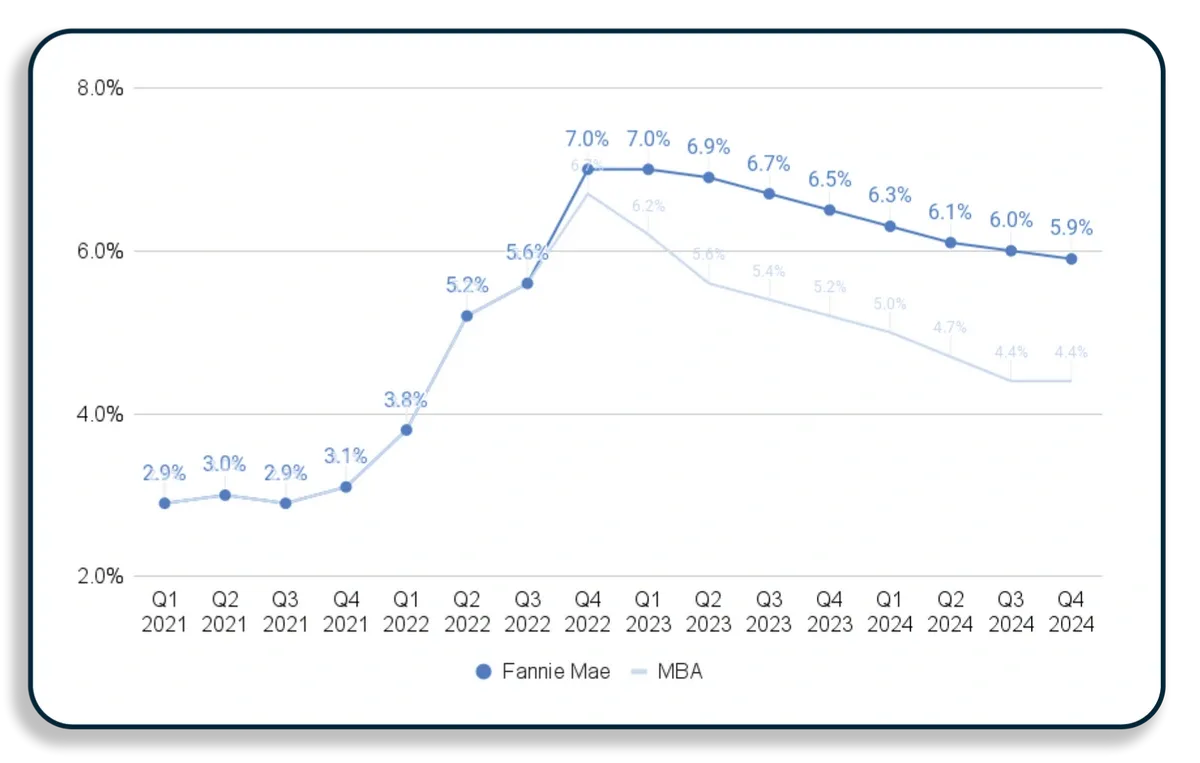

Fannie Mae and MBA Mortgage Rate Forecasts

Source: Inman News

Fannie Mae forecasters are expecting a modest recession next year and a slow, steady decline in mortgage rates over the next two years, with rates for 30-year fixed-rate loans dropping below 6 percent in late 2024. While the Mortgage Bankers Association predicts mortgage rates will fall to 5.4% at the end of 2023 and is forecasting we will be averaging 4.4% in the second half of 2024.

PRO TIP: Learn more about how buyers and sellers can win with 2-1 Buydowns. It may be possible to negotiate a rate “buydown” paid by the seller. This seller concession can reduce the amount you need to pay each month. Many sellers prefer this to reducing the sale price of their home. When rates fall in the future, you may be able to refinance to a lower rate.

The great recession had too few buyers, and the forecasted 2023 recession will likely have too few sellers, which may prevent home values from plummeting. Higher interest rates will continue to temper demand while historically lower inventory, coupled with the demographically-driven demand of Millennials, will help keep pressure on prices. Which force will win out? Time will tell as mortgage rates respond to inflation, but it’s going to be a frigid market for a while.

If you are feeling stuck or worried right now about what’s happening between inflation, mortgage rates, and the housing market – work with an expert who can help guide you from where you are today to where you want to be.

Follow us on social media for breaking market updates, graphics, videos, and more @realtysanantonio, and subscribe to our market newsletter by clicking sign up in the top right corner of our website.

Related Articles

to Top